- Home

- > Investor Relations

- > Financial Information

- > Financials

Financial Information

Financials

Final Results Announcement For The Year Ended 31 December 2025

Financials Archive![]() Note: Files are in Adobe (PDF) format.

Note: Files are in Adobe (PDF) format.

Please download the free Adobe Acrobat Reader to view these documents.

Final Results Announcement For The Year Ended 31 December 2025

Consolidated Statement Of Profit Or Loss And Other Comprehensive Income

For the year ended 31 December 2025

Consolidated Statement Of Financial Position

At 31 December 2025

BUSINESS REVIEW

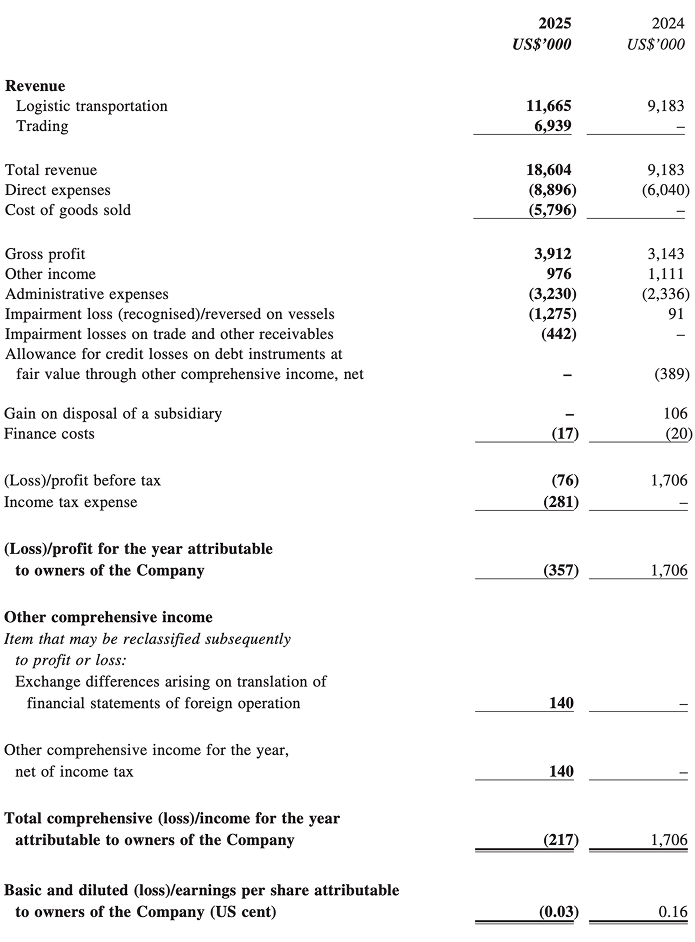

The Group has been principally engaged in logistic transportation and trading businesses during the year ended 31 December 2025 ("FY2025"). In FY2025, the Group recorded an increase in revenue by 102.6% year-on-year to US$18,604,000 (2024: US$9,183,000), mainly due to the increase in revenue of the logistic transportation business by US$2,482,000, an increase of 27% year-on-year, and the newly launched trading business's contribution of US$6,939,000. Despite the increase in revenue, there was a loss attributable to owners of the Company of US$357,000 (2024: profit of US$1,706,000) for FY2025, which was mainly due to a non-cash impairment loss on the bulkers of the Group in FY2025. Basic loss per share was US0.03 cent for FY2025 (2024: basic earnings per share of US0.16 cent). The Group remained debt free as at year ended 31 December 2025.

Logistic transportation

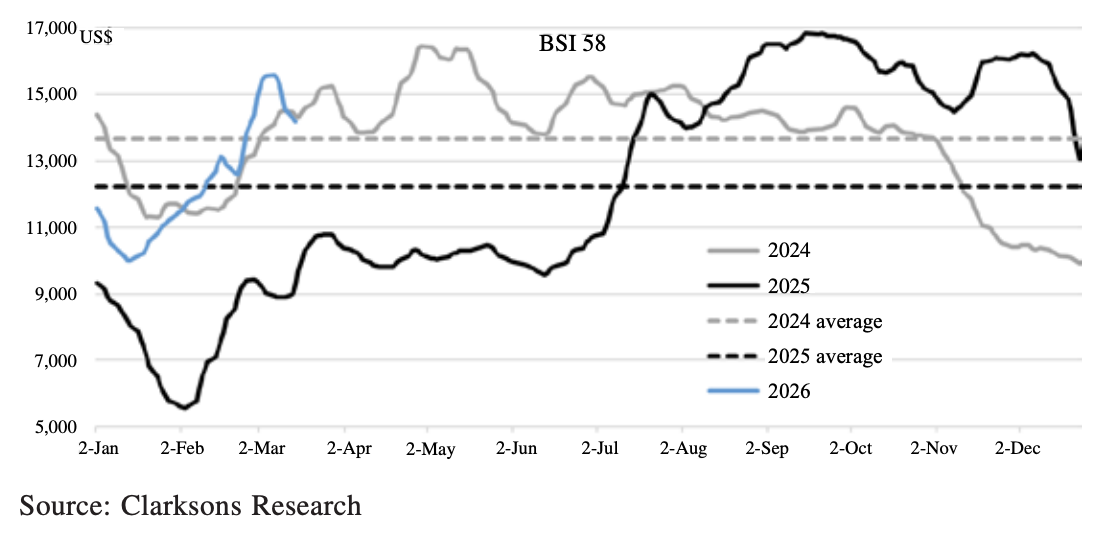

During FY2025, the dry bulk freight markets experienced a significant plunge to a historical trough in 1Q2025. Baltic Supramax Index ("BSI") recorded a five-year low of US$5,575 on 3 February 2025, after Lunar New Year and gradually gained its upward momentum since then, with a significant upward momentum by July 2025 and into 2H2025, on the back of long-haul bauxite trade from Guinea to China and a surge in export of semi-processed goods from China to emerging market in Atlantic, despite the US-Sino trade conflict and disruptions in the Red Sea. By the same token, from the supply-side, the tightened growth of dry bulk fleet of 3% net in 2025 of which 3.5% of newbuilding per Clarksons Research has escalated the upward swing of BSI in 2H2025. The newbuild pipeline in 2025 was constrained by limited available shipyard capacity and high newbuild prices, together with the launching of special port fees penalizing China made bulkers by the United States of America. Low level of newbuild coupled with uncertainty over the US-Sino trade and political tensions has driven a surge in freight rate in 2H2025. Despite the strong rebound of BSI in 2H2025, the whole year average recorded at a gross of US$12,223 in 2025, which is 10.1% year-on-year lower than that of US$13,601 in 2024.

Though market fundamentals had been tough ahead of the Group, the Group's time-chartered marine logistic transportation business significantly outperformed the drop in average BSI in FY2025. The revenue of time-chartered marine logistic transportation business segment increased to US$11,665,000 in 2025 from US$9,183,000 in 2024, an increase of 27% year-on-year, which was primarily driven by management renegotiation of more favourable freight rates with individual charterer of our fleet.

With reference to prevailing market conditions (taking into considerations of second-hand prices of comparable bulkers in terms of countries of built, deadweight tonnages, ages and market freights), in FY2025, the Group recognised a non-cash impairment loss of US$1,275,000 on bulkers (2024: a reversal of impairment loss on bulkers of US$91,000).

During FY2025, the Group expanded its logistic transportation to land from marine, by acquiring mining trucks in Mongolia at a consideration of US$5,000,000, as announced by the Company on 6 October 2025. This acquisition was completed on 31 December 2025. During FY2025, no revenue was recognised by the newly acquired mining trucks.

Trading

As stated in the 2025 interim report of the Company, due to the complex and uncertain impacts of trade war tensions and geopolitical conflicts, the global bulk shipping market was volatile and uncertain. To address the adverse impact of uncertainty on the Group, the Group actively explored and implemented business diversification. Capitalizing on the new controlling shareholder's extensive experience and business networks in coal and commodities, the Group has expanded into coal trading since 2Q2025, The Group recorded a revenue of US$6,939,000 (2024: nil) and a gross profit of US$1,143,000 (2024: nil) in 2025. In this year, the Group recorded coal trading of approximately 60,000 tons (2024: nil).

FINANCIAL REVIEW

Liquidity, financial resources and capital structure

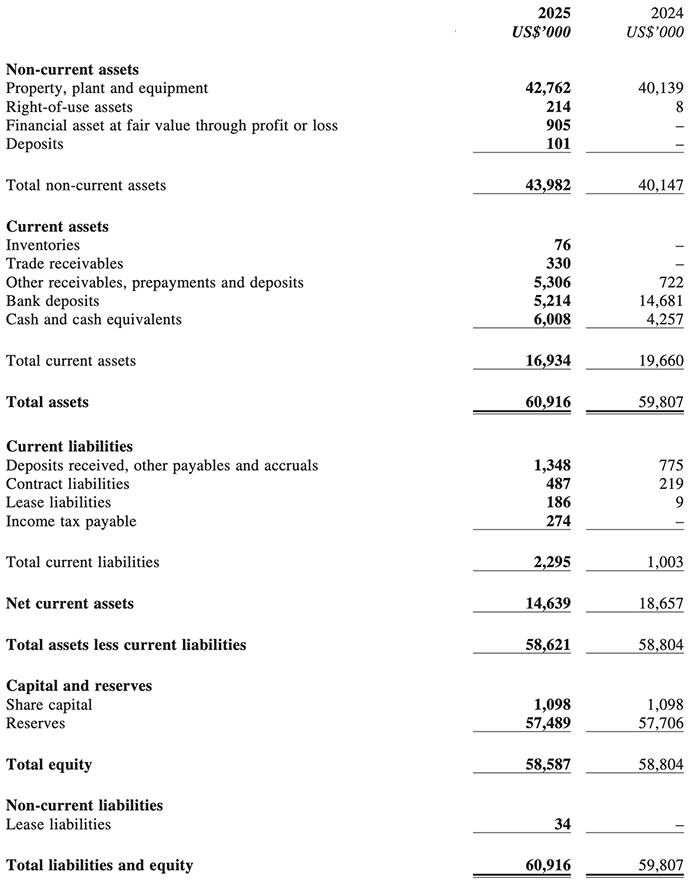

During FY2025, the Group financed its operation by cash generated from operations as well as shareholders' funds. At 31 December 2025, the Group had current assets of US$16,934,000 (2024: US$19,660,000) and liquid assets comprising bank deposits and cash and cash equivalents totaling US$11,222,000 (2024: US$18,938,000). The Group's current ratio, calculated based on current assets over current liabilities of US$2,295,000 (2024: US$1,003,000), declined to about 7.4 (2024: 19.6) at the year end. The significant decrease in current ratio was mainly attributable to an initial outlay of mining trucks in Mongolia of US$5,000,000, long-term strategic fund investment of US$900,000 and dry-docking costs, which in turn led to the decrease in bank balances whereas there is corporate income tax incurred for the Group's coal trading business in Chinese Mainland of US$281,000, which in turn led to an increase of current liabilities for the Group.

At 31 December 2025, the equity attributable to owners of the Company amounted to US$58,587,000 (2024: US$58,804,000), slightly decreased by US$217,000 when compared with the last year end and was mainly a result of the loss incurred by the Group of US$357,000 (2024: profit of US$1,706,000).

For FY2025, the Group's finance costs of US$17,000 (2024: US$20,000) represented interests on lease liabilities. Decrease in finance costs by 15% was mainly a result of the full repayment of borrowings in prior year.

At 31 December 2025, the Group's gearing ratio was zero (2024: zero).

The Group's interest income from banks decreased by 67% to US$253,000 (2024: US$776,000) over last year, mainly resulted from the decline of fixed deposit investment in banks and the general fall of bank interest rates for FY2025.

With the amount of liquid assets on hand, the management is of the view that the Group has sufficient financial resources to meet its ongoing operational requirements.

PROSPECTS

The Group maintains a cautiously optimistic view on the medium- to long-term prospects of its shipping business. The gradual easing of tariff wars and the recovery of global trade, particularly the growth of emerging markets, are driving demand for commodities. In particular, the significant increase in bulk cargo such as steel, used cars and construction vehicles, passenger and freight cars, and wind power equipment in Chinese Mainland, as the world's factory, is providing momentum for the dry bulk shipping market. However, the industry also faces new challenges, including geopolitical instability, fuel price volatility, and uneven global economic recovery.

The Board will adopt a strategy of strengthening its core business while increasing business diversification, further intensifying efforts to reduce costs and improve efficiency, and seizing opportunities to expand the fleet through acquisitions, leasing, mergers, and acquisitions to increase the scale of its shipping business. Simultaneously, the Group will actively expand its logistic transportation and trading businesses, seeking potential investment and acquisition opportunities to promote sustainable growth and maximize shareholder benefits.